|

1

|

|

|

2

|

|

|

3

|

- We the People of the United

States, in Order to form a more perfect Union, establish Justice, insure

domestic Tranquility, provide for the common defense, promote the

general Welfare, and secure the Blessings of Liberty to ourselves and

our Posterity, do ordain and establish this Constitution for the United

States of America.

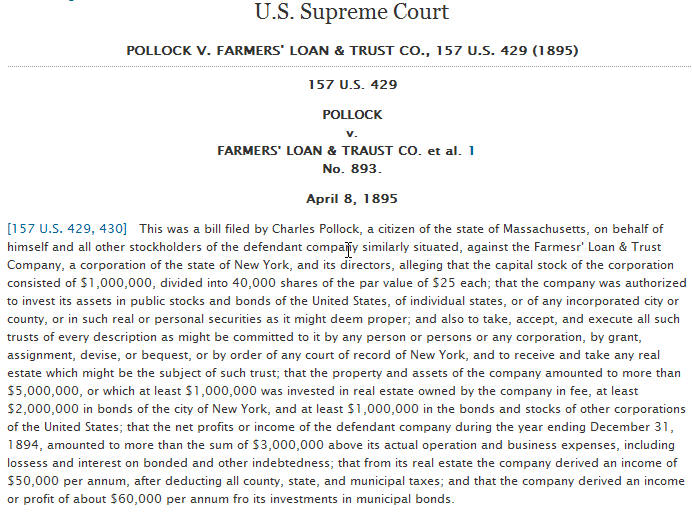

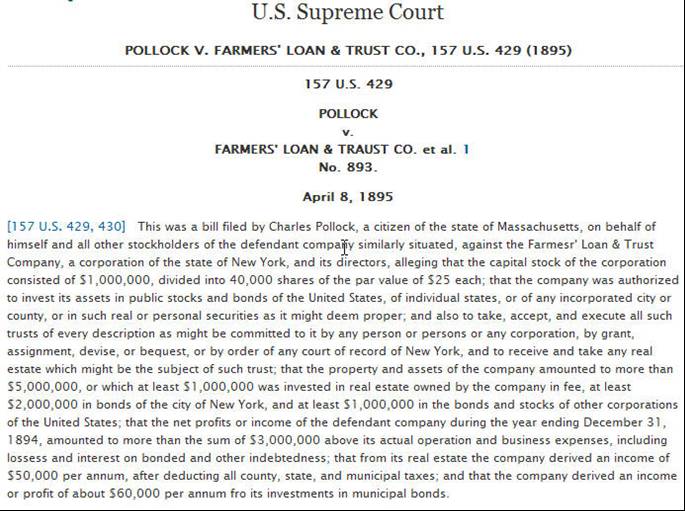

|

|

4

|

|

|

5

|

- The Constitution of the United

States of America absolutely prohibits the federal government from demanding

money directly from We The People as tax!

|

|

6

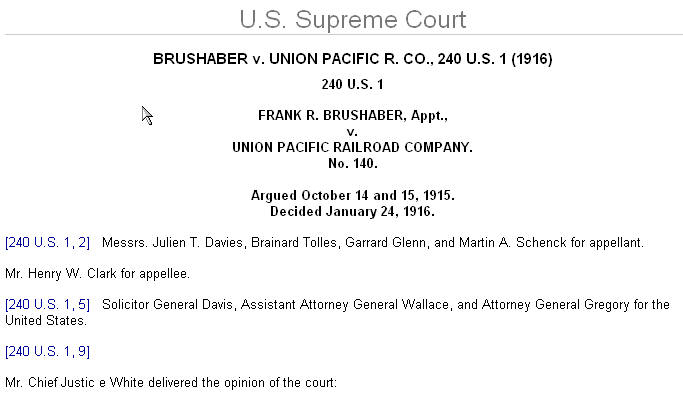

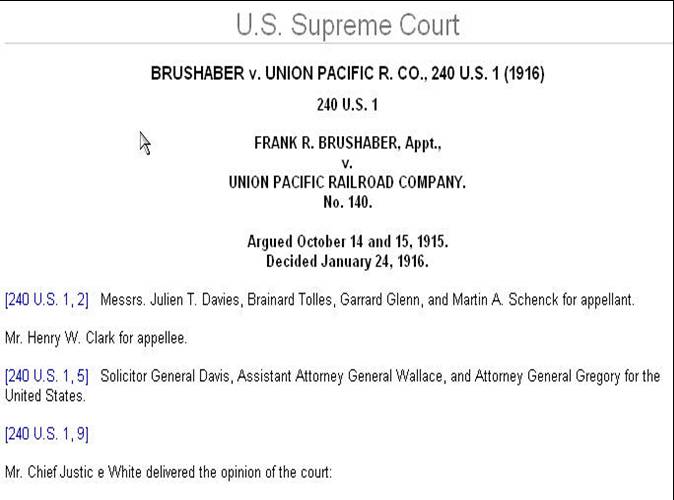

|

|

|

7

|

-

Article 1, Section 2, Clause 3

-

"Representative and direct taxes shall be apportioned among

the several states which may be included within this union, according to

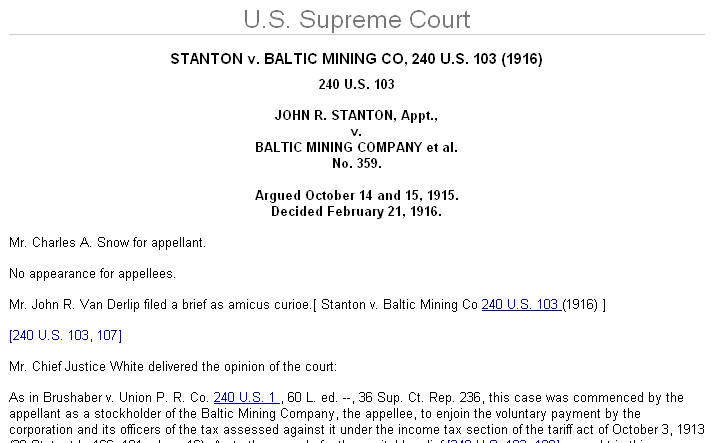

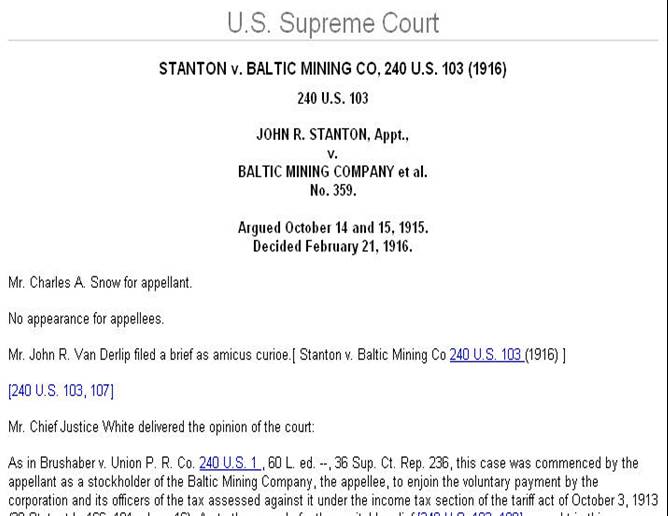

their respective numbers"

- THIS PROVISION HAS NEVER BEEN REPEALED !

|

|

8

|

- Article 1, Section 9, Clause 4

-

"No capitation or other direct tax shall be laid, unless in

proportion to the census or enumeration herein before directed to be

taken."

- THIS TOO, HAS NEVER BEEN REPEALED !

|

|

9

|

- According to the Constitution, direct taxes

must be laid in proportion to the census,

and apportioned to the States for collection.

- This means that the States pay their proportionate share of any direct

tax,

from their Treasuries; and that the citizens do NOT pay any

direct tax to the federal government from their own pockets.

|

|

10

|

- These provisions of the Constitution have never been repealed or

amended. They still today, absolutely prohibit the federal government

from taxing the people directly.

|

|

11

|

|

|

12

|

|

|

13

|

- but all duties, imposts and excises shall be uniform throughout the

United States;

|

|

14

|

- INDIRECT TAXES

ARE UNIFORM !

- DIRECT TAXES ARE

APPORTIONED

(Proportionately,

TO THE STATES

for collection !)

|

|

15

|

- And, the Constitution also

gives

the federal government a lawful authority and full jurisdiction

over all foreign affairs and matters involving foreign countries, and

over foreign persons in the United States until they become citizens.

|

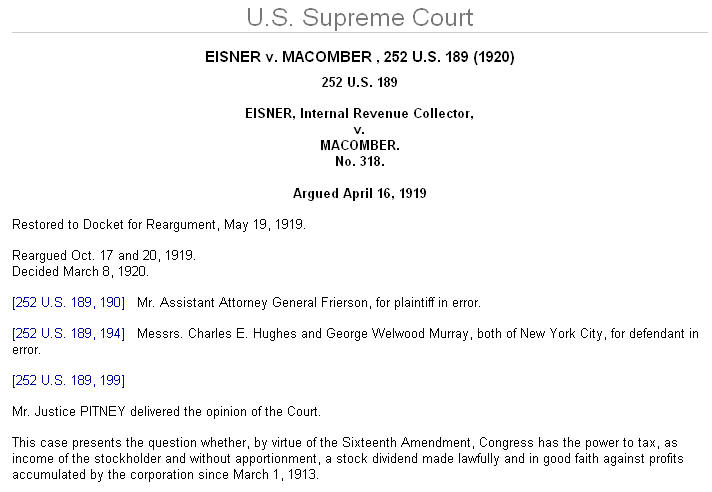

|

16

|

- The Congress shall have power …

- To regulate commerce with foreign nations, and among the several states,

and with the Indian tribes;

- To establish a uniform rule of naturalization …

- To coin money, regulate the value thereof, and of foreign coin, …

|

|

17

|

- In 1896, the Supreme Court relied upon these clauses of the Constitution

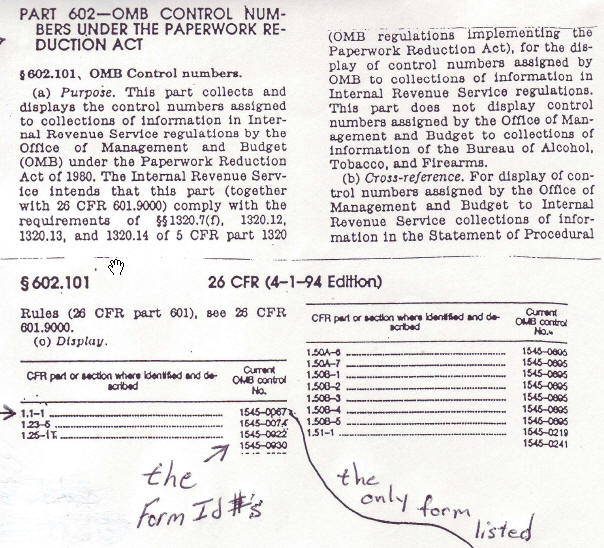

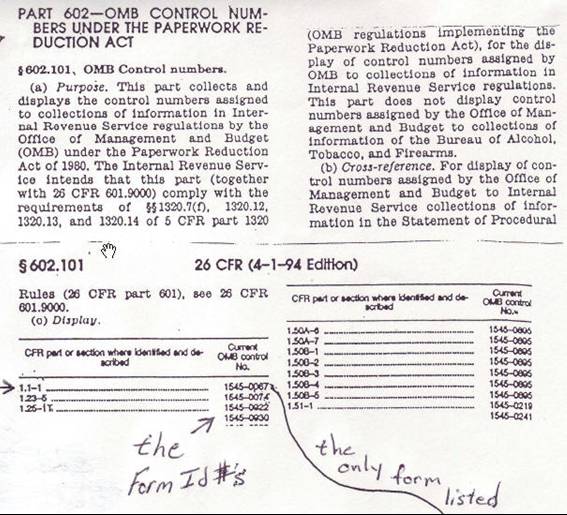

to strike down as unconstitutional an act attempting to impose directly

a graduated income tax on the earnings of American citizens from various

sources.

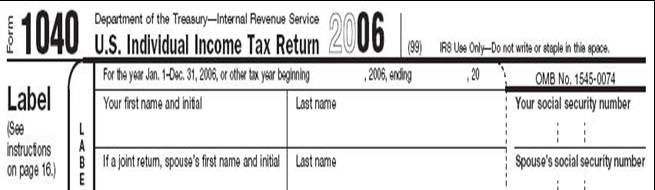

- The case is Pollock v. Farmer’s Loan & Trust Co., wherein the Court

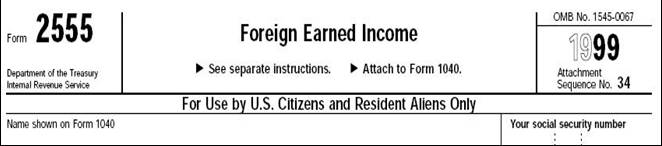

stated:

|

|

18

|

|

|

19

|

- “… it is apparent (1) that the distinction between direct and indirect

taxation was well understood by the framers of the constitution and

those who adopted it; (2) that, under the state system of taxation, all

taxes on real estate or personal property or the rents or income

thereof were regarded as direct taxes;”

|

|

20

|

- "... a tax upon property holders in respect of their estates,

whether real or personal, or of the income yielded by such estates, and

the payment of which cannot be avoided, are direct taxes ..."

Pollock v. Farmer’s Loan & Trust Co., 157 U.S. 429, 558

(1895)

|

|

21

|

- “We are of opinion that the law

in question, so far as it levies a tax on the rents or income of real

estate, is in violation of the constitution, and is invalid.”

|

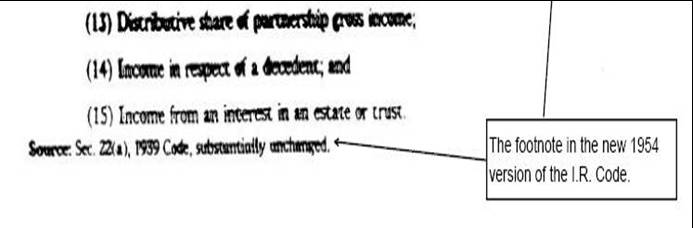

|

22

|

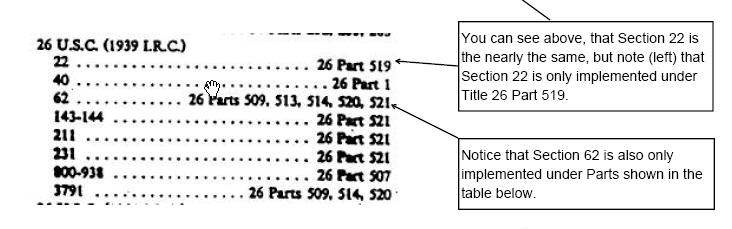

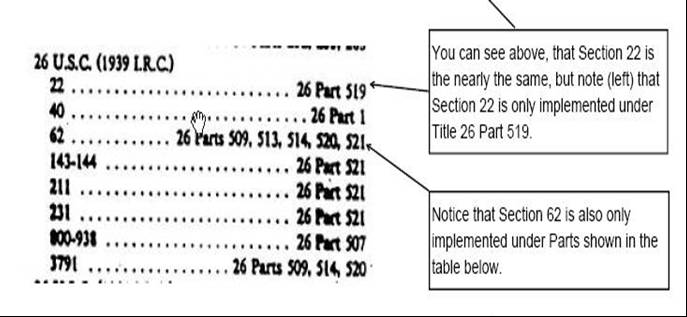

- “I am of opinion that the whole law of 1894 should be declared void, and

without any binding force, - that part which relates to the tax on the

rents, profits, or income from real estate, that is, so much as

constitutes part of the direct tax, because not imposed by the rule of

apportionment according to the representation of the states, as

prescribed by the constitution;” Pollock

v. Farmer’s Loan & Trust Co., 157 U.S. 429, 608 (1895)

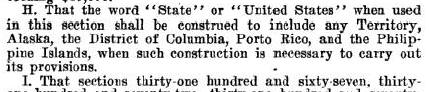

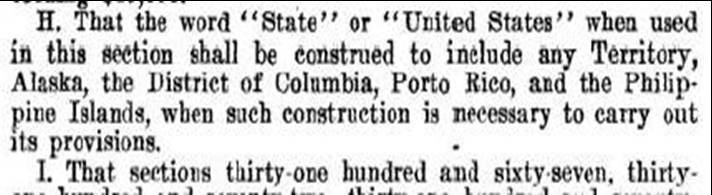

|

|

23

|

- and that part which imposes a tax upon the bonds and securities of the

several states, and upon the bonds and securities of their municipal

bodies, and upon the salaries of judges of the courts of the United

States, as being beyond the power of congress;

|

|

24

|

- and that part which lays duties, imposts, and excises, as void in not

providing for the uniformity required by the constitution in such cases”

Pollock v. Farmer’s Loan & Trust Co., 157 U.S. 429, 608

(1895)

|

|

25

|

- Thus, the income tax tested by the Supreme Court in 1896 was deemed to

be unconstitutional and was stricken down, for all of these identified

constitutional “problems” with the legislation.

|

|

26

|

|

|

27

|

- “Congress shall have power to

lay and

collect taxes on income, from whatever source derived, without

apportionment among the several states, and without regard to any census

or enumeration.”

- ADOPTED IN 1913.

- DID THIS CHANGE EVERYTHING ?

|

|

28

|

- DOES THE 16th AMENDMENT REPEAL, ALTER, AMEND, or DESTROY THE

PRE-EXISTING PROVISIONS OF ARTICLE 1 regarding direct taxation we have

just reviewed (1,2,3 & 1,9,4)?

- DOES IT OVERCOME THE POLLOCK RULING BY CREATING A NEW FEDERAL POWER TO

DIRECTLY

TAX THE CITIZENS ?

|

|

29

|

- “Congress shall have power to

lay and collect taxes on income, from whatever source derived, without

apportionment among the several states, and without regard to any census

or enumeration.”

- DOES THIS ACTUALLY SAY THAT THE INCOME TAX IS A DIRECT TAX ? (Does it

contain the word “direct” ?)

- NO ! IT DOES NOT !

|

|

30

|

- Now, the U.S. government wants you to believe that the 16th

Amendment gives the I.R.S. (government) additional taxing powers that

did not exist before its adoption in 1913.

- BUT, according to the Supreme Court

- THAT’S NOT TRUE !

|

|

31

|

- SINCE 1916, however, the inferior district and circuit federal courts

have just plain lied to the American People and claimed that the Supreme

Court determined in the Brushaber v. Union Pacific R.R. Co. case of

1916, that:

- “The Sixteenth Amendment authorizes

a direct nonapportioned tax upon United States citizens throughout the

nation". United States v. Collins, 920 F.2d 619, 629 (10th

Cir. 1990)

- BUT, this statement and claim

IS A BALD FACED LIE

|

|

32

|

- The SUPREME Court’s decision taken in the Brushaber case absolutely did

not say that the 16th Amendment authorizes a direct nonapportioned tax,

because that would have engineered a direct and inherent conflict within

the Constitution itself, with those pre-existing Article I clauses prohibiting direct taxation!

- (Article 1, Section 2, Clause 3, and

- Article 1, Section 9, Clause

4)

|

|

33

|

- The SUPREME Court knew in 1916 that it is not a legitimate application

of the law to use one provision of the law to destroy another.

(Who knows what they know now!)

- Provisions of the law of equal stature should peacefully and

harmoniously co-exist with one another, and should never be interpreted

to be in direct conflict with each other, or to destroy one another.

- Otherwise, you will have arbitrary and capricious applications of the

conflicting provisions of the laws offered up by everyone from Grandma

to Judge Judy.

|

|

34

|

- However, the Supreme Court did decide and state in the Brushaber and Stanton

case opinions in 1916, that the income tax legislation enacted in 1913

and tested by the court in those cases, is constitutional.

- WHY DID THEY TAKE THIS DECISION ?

|

|

35

|

- SO, JUST WHAT DID THE SUPREME

COURT REALLY SAY ABOUT THOSE INCOME TAX LAWS IT ACTUALLY TESTED, IN

THOSE FIRST INCOME TAX DECISIONS, IN 1916 ?

|

|

36

|

|

|

37

|

- “We are of opinion, however, that the confusion is not inherent, but rather

arises from the conclusion that the

16th Amendment provides

for a hitherto unknown power of taxation; … “

|

|

38

|

- “… that is, a power to levy an income tax which, although direct, should

not be subject to the regulation of apportionment applicable to all

other direct taxes. And the far-reaching effect of this erroneous

assumption will be made clear…”

Brushaber v. Union Pacific R.R., 240 U.S. 1, 11 (1916)

|

|

39

|

- “…it clearly results that the proposition and the contentions

under it, if acceded to, would cause one provision of the Constitution

to destroy another; that is, they would result in bringing the

provisions of the Amendment exempting a direct tax from apportionment into

irreconcilable conflict with the general requirement that all direct

taxes be apportioned.”

[Brushaber v. Union Pac. R.R., 240 U.S. 1, 12]

|

|

40

|

- “... This result … would create radical and destructive changes in our

constitutional system and multiply confusion”

- [Brushaber v. Union Pac. R.R.,

240 U.S. 1, 12]

- (Did they see it coming, or

what ?)

|

|

41

|

- The Supreme Court reaffirms, and makes absolutely clear, the true nature

of their ruling on the income tax legislation enacted in 1913, in the

opinion of the very next case they publish after the Brushaber case in

1916.

- Stanton v. Baltic Mining Co.

|

|

42

|

|

|

43

|

"...by the previous ruling (Brushaber), it was settled that the

provisions of the 16th Amendment conferred no new power of taxation…”

|

|

44

|

- “…but simply prohibited the

previous complete and plenary power of income taxation possessed by

Congress from the beginning from being taken out of the category of

INDIRECT taxation to which it inherently belonged.“

Stanton v. Baltic Mining Co., 240 US 103 (1916)

|

|

45

|

- So, in 1916 the Supreme Court said that the income tax is Constitutional

because it is an INDIRECT tax, NOT a direct tax.

- SO, what kind of INdirect tax is

it: impost, duty, or excise ?

|

|

46

|

- Well, what “form(s)” did income

tax(es) take previously, under this “previous, complete and plenary

power” to tax income that the Supreme Court identifies in Stanton, and,

that existed before the 16th Amendment?

|

|

47

|

- SEC. 89 And be it further enacted, That for the purpose of modifying and

reenacting, as hereinafter provided, so much of an act, entitled

"An act to provide increased revenue from imports to pay interest

on the public debt, and for other purposes," approved fifth of

August, eighteen hundred and sixty-one, as relates to income tax;...

|

|

48

|

- SEC. 86 And be it further enacted, that on and after the first day of

August, eighteen hundred and sixty-two, there shall be levied,

collected, and paid on all salaries of officers, or payments to persons

in the civil, military, naval, or other employment or Service of the

United States, including

|

|

49

|

- (including) senators and representatives and delegates in Congress, when

exceeding the rate of six hundred dollars per annum, a duty of three per

centum on the excess above the said six hundred dollars; and it shall be

the duty of all paymasters, and all disbursing officers

|

|

50

|

- when making any payments to

officers and persons as aforesaid, or upon settling or adjusting the

accounts of such officers and persons, to deduct and withhold the

aforesaid duty of three per centum, and shall, at the same time, make a

certificate stating the name of the officer or person from whom such

deduction was made, and the amount thereof, which shall be transmitted

to the office of the Commissioner of Internal Revenue

|

|

51

|

- “… it was settled in Stratton's

Independence v. Howbert, 231 U.S. 399, 58 L. ed. 285, 34 Sup. Ct. Rep.

136, that such tax is not a tax upon property as such because of its

ownership, but a true excise levied on the results of the business of

carrying on mining operations. (pp. 413 et seq.)” Stanton v. Baltic Mining Co., 240 US

103, 114 (1916)

|

|

52

|

- “The act of 1909 avoided this

difficulty by imposing not a [direct] income tax, but an excise tax upon

the conduct of business in a corporate capacity, measuring, however, the

amount of tax by the income of the corporation,

|

|

53

|

|

|

54

|

- So, if according to the Supreme Court a direct income tax was unconstitutional

before the 16th Amendment (Pollock), and

- No new powers of taxation were created or conferred by the adoption of

the Amendment (Stanton), then

- HOW CAN A DIRECT TAX ON INCOME BE CONSTITUTIONAL AFTER THE 16th

Amendment ?

(Clearly, honestly, it can’t be !)

|

|

55

|

- As THE COURT SAID IN THE STANTON

DECISION THAT THE INCOME TAX BEING TESTED IN THAT CASE IS CONSTITUTIONAL

BECAUSE IT WAS NOT IMPOSED AS A DIRECT TAX, BUT AS AN INDIRECT TAX IN

THE FORM OF AN EXCISE !

|

|

56

|

|

|

57

|

- “Excises are taxes laid

upon: the manufacture, sale or

consumption of commodities within the country, upon licenses to pursue

certain occupations, and upon corporate privileges;

|

|

58

|

- “the requirement to pay such

taxes involves the exercise of the privilege and if business is not done

in the manner described no tax is payable...it is the privilege which is

the subject of the tax and not the mere buying, selling or handling of

goods.”

|

|

59

|

- THE INCOME TAX UPHELD IN STANTON,

WAS UPHELD AS AN INDIRECT EXCISE TAX ON CORPORATIONS THAT CANNOT BE

APPLIED TO THE INCOME OF AN AMERICAN CITIZEN BECAUSE THE CITIZEN ENJOYS

NO TAXABLE CORPORATE PRIVILEGES.

|

|

60

|

- Flint v Stone Tracy is

cited by the Supreme

Court more than 600

times as the controlling precedent in subsequent cases concerning

excise taxation. 600 Times !

|

|

61

|

- So, what did the Supreme Court really

tell us about the income tax in that first decision in 1916, Brushaber

v. Union Pacific R.R. Co. ?

|

|

62

|

- In the very first sentence of the decision the Court says:

- “As a stockholder of the Union

Pacific Railroad Company, the appellant filed his bill to enjoin the

corporation from complying with the income tax provisions of the tariff

act of October 3, 1913.”

|

|

63

|

- A tariff is one form of an IMPOST!

A tariff is a FOREIGN tax imposed on foreign goods entering the

country, or imposed on foreign activity occurring within the country, BUT

IT IS NOT A TAX THAT CAN EVER BE IMPOSED ON ANY DOMESTIC earnings of the

citizens.

|

|

64

|

- I REPEAT:

A tariff is an indirect tax in the form of an impost, (under

Article 1, Sec. 8, Clause 1 of the Constitution, not the 16th

Amendment), in the form of a FOREIGN TAX THAT BY DEFINITION IS NEVER IMPOSED ON THE DOMESTIC ACTIVITY

OF THE AMERICAN CITIZENS IN THE FIFTY STATES !

|

|

65

|

- This is why the Supreme Court

said that the income tax powers of the tariff legislation tested in 1913

were a power “previous complete and plenary … possessed by Congress from

the beginning”, and was prevented “from being taken out of the category

of INDIRECT taxation to which it inherently belonged.“

Stanton v. Baltic Mining Co., 240 US 103 (1916)

|

|

66

|

- Because the corporate income tax

is laid as an indirect excise

under Article 1, Section 8, Clause 1 (which under Flint v Stone

Tracy citizens cannot be subjected to), and the personal income tax is

laid

|

|

67

|

- AS A TARIFF, one form of an

impost, which is also an indirect tax under Article 1, Section 8, Clause

1, and which plenary power to tax

(the income of foreigners and corporations) existed under the

Constitution from the beginning, AS AN INDIRECT POWER.

IT HAS NOTHING TO DO

WITH THE 16TH AMENDMENT !

|

|

68

|

"...by the previous ruling (Brushaber), it was settled that the

provisions of the 16th Amendment conferred no new power of taxation…”

|

|

69

|

- ”The Sixteenth Amendment,

although referred to in argument, has no real bearing and may be put out

of view. As pointed out in recent decisions, it does not extend the

taxing power to new or excepted subjects, … Brushaber v. Union Pacific

R.R. Co., 240 U.S. 1, 17-19; Stanton v. Baltic Mining Co., 240 U.S. 103,

112-113."

|

|

70

|

- “As repeatedly held, this [the

16th Amendment] did not extend the taxing power to new subjects,… . Brushaber

v. Union Pacific R.R. Co., 240 U.S. 1, 17-19; Stanton v. Baltic Mining

Co., 240 U.S. 103, 112 et seq.; Peck & Co. v. Lowe, 247 U.S. 165,

172-173.

|

|

71

|

- Is there any evidence of the foreign nature of this tariff (the income

tax) present in the income tax law(s) ?

- Then in 1913 ? NOW in 2008 ???

- Does the Supreme Court tell us anything else useful about the

income tax legislation being

tested in the Brushaber case ?

|

|

72

|

- YES! The Supreme Court

tell us in the Brushaber decision:

“2. The act provides for

collecting the tax at the source; that is, makes it the duty of

corporations, etc., to retain and pay the sum of the tax …”

Brushaber v. Union Pacific R.R. Co, 240 US 1, 21-22 (1916).

|

|

73

|

- “makes it the duty

of corporations,

etc.,

to retain and pay

the sum of the tax”

|

|

74

|

- This is, of course, what the income tax legislation was really all about

in 1913 – “collection at the source”; getting the tax dollars (the

money) from the taxpayer before it was all spent, and could therefore no

longer be collected as tax, or because the taxpayer himself was no

longer approachable because he had left the area (or the country?).

|

|

75

|

- Therefore, the “duty”, identified

by the Supreme Court to “retain and pay the sum of the tax“, was (and

still is) defined in the law as the duty of the “Withholding Agent” to withhold income taxes from all

persons identified in the law as being subject to the withholding of

tax.

|

|

76

|

- (a)(16) Withholding Agent. The term ''Withholding Agent'' means any

person required to deduct and withhold any tax under the provisions of

sections 1441, 1442, 1443, or 1461.

|

|

77

|

- So, under the law, who

do “Withholding Agents” withhold income tax from ?

|

|

78

|

- (a) General rule. Except as otherwise provided in

subsection (c) all persons, in

whatever capacity acting having the

control, receipt, custody, disposal or payment of any of the items of income specified

in subsection (b) (to the extent that any of such items constitutes gross

income from sources within the United States), of any nonresident alien individual, or of

any foreign partnership shall deduct and withhold from such items a tax

equal to 30 percent thereof, except that

in the case of any items of income specified in the second

sentence of subsection (b), the tax shall be equal to 14 percent of such

item. (emphasis added)

|

|

79

|

- (b) Income items The items of income referred to in subsection (a) are interest

… dividends, rent, salaries, wages, premiums, annuities, compensations,

remunerations, emoluments, or other fixed or determinable annual or

periodical gains, profits, and income, gains described in section 631

(b) or (c), amounts subject to tax under section 871 (a)(1)(C), gains

subject to tax under section 871 (a)(1)(D) …

|

|

80

|

- (a) General rule. In the case of foreign corporations

subject to taxation under this subtitle, there shall be deducted and

withheld at the source in the same manner and on the same items of

income as is provided in Section

1441 a tax equal to 30% thereof …

|

|

81

|

- (b) Income subject to section 4948. In the case of income of a foreign

organization subject to the tax imposed by section 4948 (a), this

chapter shall apply, except that the deduction and withholding shall be

at the rate of 4 percent and shall be subject to such conditions as may

be provided under regulations prescribed by the Secretary.

|

|

82

|

- § 7701 Definitions.

- (a) When used in this Title

...

- (1). Person. – The term “person” shall be

construed to mean and include an individual, a trust, estate,

partnership, association, company or corporation.

|

|

83

|

- One should carefully note that the laws (Sec. 1441, 1442, 1443), by

virtue of the definition of the Withholding Agent, ONLY authorize the

withholding of income tax from FOREIGN “persons”, and then remember that

the Supreme Court said that the income tax of 1913 was part of a tariff

act (that by definition can only be imposed on foreign activity).

|

|

84

|

- And, under the law, who is made liable for payment of the income tax ?

|

|

85

|

- “Every person required to

deduct and withhold any tax under this chapter is hereby made liable for

such tax and is hereby indemnified against the claims and demands of any

person for the amount of any payments made in accordance with the

provisions of this chapter.”

|

|

86

|

- This is the ONLY statute in all

of Subtitle A that makes anyone liable for the payment of the income

tax, and it makes only the “Withholding Agents” liable for tax that they

have collected. BUT NOT FOR TAX

ON WHAT THEY HAVE EARNED!

|

|

87

|

- By making ONLY the Withholding Agents liable as tax collectors for the

payment of tax that has been collected, the entire scheme of the income

tax is kept INDIRECT.

|

|

88

|

- By injecting this third party

into the scheme for the collection at the source of the income tax, the burden

to pay the tax is shifted from the payor of the tax - the tax collector,

the “corporations, etc.”, (the Withholding Agents); the burden is

shifted by withholding to the actual taxed subjects and only true

taxpayers – the non-resident aliens and foreign corporations, the “persons” that are the proper subjects of a

tariff.

|

|

89

|

- “taxes paid primarily by persons

who can shift the burden upon someone else, …, are considered indirect

taxes;”

Under the enacted legislation, Withholding Agents shift the

burden of the tax to the foreigners from whom they withhold.

|

|

90

|

- And so we see that Congress

(or the authors of the original income tax legislation, whoever they may

be) actually, very carefully crafted these income tax laws, and the

entire scheme for the collection of the tax at the source, to be

constitutional by writing the law specifically as they were instructed

to write it by the Supreme Court in 1896 when it struck down the 1895

legislation as un-constitutionally direct because it did not provide for

shifting the burden of the tax, but attempted to lay and collect the tax

directly.

|

|

91

|

- We the People are NOT the subjects of the federal government. THE SUBJECTS ARE THE FOREIGN PERSONS

in the United States !

- We The People are the Sovereign, the true “owner”, authority, and power

in the nation, and the federal government is our servant, acting as our

political representative, NOT OUR RULER.

WE THE PEOPLE ARE THE MASTERS,

the federal government is

OUR SERVANT.

|

|

92

|

- SO,

SINCE WHEN

DOES THE SERVANT TAX THE MASTER?

|

|

93

|

- Sovereigns do not impose tax on themselves, but on their subjects.

- Sovereigns do NOT pay tax, THEY COLLECT IT from their subjects.

|

|

94

|

- We The People, the true sovereign, are not the intended taxpayers of

this income tax.

- Under the law we are the intended TAX COLLECTORS.

|

|

95

|

- America was established as the

First Nation of Kings, because in America it is We The People who are

collectively the national Sovereign.

We ALL hold the power of the “King”, the Sovereign, and the King

doesn’t pay tax,

HE COLLECTS IT !

|

|

96

|

- We the People are the “etc.” in the Brushaber quote cited earlier, and

- like the corporations, We The People have a duty to “retain and pay the

sum of the tax”, or

- withhold tax from the subject

foreign persons.

- This duty to pay tax (over to the Treasury) ONLY relates to the taxes

that we have withheld from other persons (the subject foreign parties).

|

|

97

|

- AMERICAN CITIZENS ARE NOT REQUIRED BY LAW TO PAY INCOME TAX ON THEIR OWN

DOMESTIC INCOME

- That would constitute DIRECT taxation without apportionment and that is

STILL UNCONSTITUTIONAL

- The provisions of Article 1 (1,2,3 & 1,9,4) have never been repealed

or amended.

- The Pollock decision has never been over-ruled!

- Direct taxation of income is still unconstitutional!

|

|

98

|

- Income tax, like any tax, can ONLY be either a direct tax, or an indirect

tax, it CANNOT BE BOTH.

- That is why there is no liability for income tax established anywhere in

the Subtitle A statutes except for Section 1461, which

- Indirectly establishes the liability of the Withholding Agents for the

tax that they have withheld from the subject foreign taxpayers.

|

|

99

|

- Having found an obvious and clearly INDIRECT implementation for the

collection of the income tax in this scheme of collection at the source

by withholding, and having found a

- Specification of liability in the name of that third party tax

collector, the Withholding Agents (but not in the name of any other

party, not even the subject foreign taxpayer), and

- Knowing that no tax can be BOTH INdirect and Direct

|

|

100

|

- We can all stop imagining that there is a direct implementation of the

income tax imposed elsewhere in the statutes -involving a so-called

mandatory requirement for citizens to perform a direct self-assessment

of their own domestic activities using a Form 1040, in violation of both

their 4th and 5th amendment rights.

- IT JUST CANNOT BE SO!

- BECAUSE THEN THE TAX WOULD BE BOTH DIRECT AND INDIRECT, and under the

Constitution, that cannot be!

- IT CAN ONLY BE ONE OR THE OTHER!

|

|

101

|

- If we accept the government’s claim that they are authorized to tax the

fruits of our labor directly, as they have been doing. What is the end result of an extension

of that power to its theoretical ends?

- The tax originated at only 1% , and people know that today’s rates are

15%, 28%, 31%, 36%, etc., and

- There is nothing we can do about it except pay the tax, because the

government holds the power to do this.

Right?

|

|

102

|

- If we take this assumed taxing power to its theoretical extreme, what is

the obvious end result when the government decides it is necessary (or

maybe just desirable) to tax the fruits of our labor at a rate of 100% -

without allowing expenses (as they do to individuals)

- IS THERE ANYTING YOU CAN DO ABOUT IT THEN? WHY?

HOW ?

- What happens if we allow this system to exist ?

- WE ARE EFFECTIVELY REDUCED TO A NATION OF SLAVES – THAT’S WHAT !

|

|

103

|

- So, before the 16th Amendment,

under the Pollock decision in 1896, the income tax on citizens is deemed

a direct tax that is not constitutional.

- After the 16th Amendment the Court says the income tax is an

indirect tax that

is constitutional as a tariff that is collected at the source by

withholding tax from payments made to subject persons, who it turns out,

are all foreign !

(And therefore, properly subjected to a tariff!)

|

|

104

|

- SO, WHAT DOES THE SUPREME COURT

AND THE LAW REALLY SAY ABOUT HOW THE INCOME TAX APPLIES

TO CITIZENS, AFTER

THE ADOPTION OF

THE 16th AMENDMENT ?

|

|

105

|

|

|

106

|

- This case presents, IN 1920, SEVEN YEARS AFTER THE ADOPTION OF THE 16th

AMENDMENT,

- “the question whether, by

virtue of the Sixteenth Amendment, Congress has the power to tax, as

income of the stockholder and without apportionment, a stock dividend

made lawfully and in good faith against profits accumulated by the

corporation since March 1, 1913 “

|

|

107

|

- “Thus, from every point of view we are brought irresistibly to the

conclusion that neither under the Sixteenth Amendment nor otherwise has

Congress power to tax without apportionment a true stock dividend made

lawfully and in good faith, or the accumulated profits behind it, as

income of the stockholder.”

- Eisner v. Macomber, 252 U.S.

189, 219 (1920)

|

|

108

|

- “ The Revenue Act of 1916, in

so far as it imposes a tax upon the stockholder because of such dividend,

contravenes the provisions of article 1, 2, cl. 3, and article 1, 9, cl.

4, of the Constitution, and to this extent is invalid, notwithstanding the

Sixteenth Amendment.”

Eisner v. Macomber, 252 U.S. 189,219

|

|

109

|

- As explained, The 16th Amendment cannot be interpreted as authorizing

the income tax as a direct tax because that interpretation of the

Constitution would engineer a direct and inherent contradiction within

the Constitution itself (the 16th

Amendment would be in direct conflict with the pre-existing provisions

of Article 1 forbidding direct taxation unless apportioned to the states

for collection, etc.).

- And that can never be allowed to happen, and the Supreme Court

understood these things in 1920.

|

|

110

|

- SO WHAT RESULT CAME

OUT OF THE BRUSHABER AND STANTON DECISIONS HANDED DOWN IN 1916 ?

|

|

111

|

- Income

Taxes

- Under the decision of the

Supreme Court of the United States in the case of Brushaber v. Union

Pacific Railway Co., decided January 21, 1916, it is hereby held that income

accruing to nonresident aliens in the form of interest from the bonds

and dividends on the stock of domestic corporations is subject to the

income tax imposed by the act of October 3, 1913.

- (Accruing to WHO ? Non-resident aliens!)

|

|

112

|

-

(Paragraph 2)

- Nonresident aliens are not

entitled to the specific exemption designated in paragraph C of the

income-tax law, but are liable for the normal and additional tax upon

the entire net income "from all property owned, and of every

business, trade, or profession carried on in the United States,"

computed upon the basis prescribed in the law.

- (Does this say Citizens are

liable ? NO!)

|

|

113

|

- Paragraph 3

- The responsible heads, agents,

or representatives of nonresident aliens, who are in charge of the

property owned or business carried on within the United States, shall

make a full and complete return of the income therefrom on Form 1040,

revised, and shall pay any and all tax, normal and additional, assessed upon

the income received by them in behalf of their nonresident alien

principals.

- WHOSE INCOME GOES ON A FORM 1040

?

- THE NON-RESIDENT ALIEN’S !!!

|

|

114

|

- AND WHAT IS

- ACTUALLY IN

- THE LAW TODAY ?

|

|

115

|

- § 1. Tax Imposed.

- (a) Married individuals filing joint returns and surviving spouses. There is hereby imposed on the taxable

income of

- (1) every married individual (as defined in Section 7703) jointly with

his spouse under Section 6013, and

- (2) every surviving spouse (as defined in Section 2(a))

- a tax determined in accordance with the following table:

- If taxable income is:

The tax is:

- Not over 32,450

15% of taxable income

- ...

- THIS SHOULD LOOK FAMILIAR ???

|

|

116

|

- NOTE that neither persons nor property are the subject of this Section 1

tax, but

“TAXABLE INCOME” is !

- NOTE that while there is a tax imposed on individuals, they are not

identified.

- NOTE that this statute does not state how the tax is to be collected, or

by whom.

- NOTE that this statute does not say how the tax is to be paid, or by

whom.

- NOTE that this statute does not say who is liable, or to be made liable,

for the payment of the tax.

|

|

117

|

- Leaving you to assume

- you are the “individual”,

- you have “taxable income”,

- you must file a return reporting

such,

- you are liable for the tax

imposed,

- you must pay the tax yourself.

|

|

118

|

|

|

119

|

- PART 602 - OMB CONTROL NUMBERS UNDER

THE

PAPERWORK REDUCTION ACT

- Section 602.101. OMB Control

numbers.

- (a) Purpose.. This part

collects and displays the control numbers assigned to collections of

information in Internal Revenue Service regulations by the Office of

Management and Budget (OMB) under the Paperwork Reduction Act of

1980. The Internal Revenue

Service intends that this part comply with the requirements of .... (OMB

regulations implementing the Paperwork Reduction Act), for the display

of control numbers assigned by OMB to collections of information in

Internal Revenue Service regulations....

|

|

120

|

- 26 CFR (4-1-94 Edition)

- CFR part or section where

Current

- identified and described OMB Control No.

- 1.1-1 ........................................... 1545-0067

- 1.23-5 ...........................................1545-0074

- 1.25-1T..........................................1545-0922

-

1545-0930

- 1.25-2T..........................................1545-0922

- .....

- Section 1 (the Tax Imposed) requires the form bearing OMB Control Number

1545-0067.

|

|

121

|

|

|

122

|

- THE OMB DOCUMENT CONTROL NUMBER ON A FORM 1040 is 1545-0074, (and is NOT

1545-0067, which is shown as required) therefore:

- FORM 1040 is NOT REQUIRED BY LAW IN ASSOCIATION WITH THE INCOME TAX

IMPOSED BY SECTION 1.

|

|

123

|

- The OMB Document Control No. 1545-0067 was assigned to Form 2555 until

2000.

- This is the form REQUIRED by law to be filed by Citizens in association

with the income tax imposed by Section 1, NOT FORM 1040!

- Reporting FOREIGN EARNED INCOME !

(under tax treaties) !

|

|

124

|

- Subtitle A - Income Taxes

chapters 1 - 6

- Subtitle B - Estate and Gift Taxes

chapters 11 -13

- Subtitle C - Employment Taxes

chapters 21 - 25

- Subtitle D – Misc. Excise Taxes

chapters 31 -47

- Subtitle E - Alcohol, Tobacco and

Other

Excise Taxes chapters 51 -

54

- Subtitle F - Procedure and Admin.

chapters 61 - 80

- Subtitle G - The Joint Comittee on Taxation

- Subtitle H - Financing of Presidential Election Campaign

|

|

125

|

- CHAPTER 1—NORMAL TAXES AND SURTAXES

- CHAPTER 2—TAX ON SELF-EMPLOYMENT INCOME

- CHAPTER 3—WITHHOLDING OF TAX ON

NONRESIDENT ALIENS AND FOREIGN

CORPORATIONS

- [CHAPTER 4—REPEALED]

- [CHAPTER 5—REPEALED]

- CHAPTER 6—CONSOLIDATED RETURNS

|

|

126

|

- NOW LET’S LOOK AT

THE LAWS AUTHORIZING

AN EMPLOYER TO WITHHOLD INCOME

TAX FROM AN EMPLOYEE !

|

|

127

|

- (a) Requirement of withholding

- (1) In general

- Except as otherwise provided in this section, every employer making

payment of wages shall deduct and

withhold upon such wages a tax determined in accordance with tables or

computational procedures prescribed by the Secretary ... (emphasis added)

|

|

128

|

- (n) Employees incurring no income tax liability

- Notwithstanding any other provision of this section, an employer shall not

be required to deduct and withhold ANY tax under this chapter upon a

payment of wages to an employee if there is in effect with respect to

such payment a withholding exemption certificate (in such form and

containing such other information as the Secretary may prescribe) furnished

to the employer by the employee certifying that the employee - …

|

|

129

|

- (n) Employees incurring no income tax liability (cont.)

- …

- (1) incurred no liability for

income tax imposed under subtitle A for his preceding taxable year, and

- (2) anticipates that he will

incur no liability for income tax imposed under subtitle A for his current taxable year.

|

|

130

|

- AND WHO WAS IT, THAT WAS MADE LIABLE

FOR INCOME TAX UNDER SUBTITLE A ?

- THE “WITHHOLDING AGENTS” !

(Under Section 1461,

remember ?)

- ACTING AS TAX COLLECTORS !

|

|

131

|

- WHY ? Because the income tax is really just

an indirect tax in the form of a tariff that is “collected at the source” by Withholding Agents, acting as tax

collectors for the U.S. government, who have a duty to “retain and pay

the sum of the tax” by withholding tax from payments made to foreign

persons.

|

|

132

|

- All exactly as identified by the

Supreme Court in 1916 when they upheld as Constitutional both the scheme

for the collection of the tax (withholding by tax collectors), and the

tax itself (as an indirect foreign tariff).

|

|

133

|

- The taxpayers are never made

directly liable by the statutes, because that would be

unconstitutionally direct taxation.

|

|

134

|

- UNDER THE ENACTED LAWS, IS THE

SCHEME FOR THE COLLECTION AND ENFORCEMENT OF THE INCOME TAX CONSISTENT

BETWEEN SUBTITLES ?

|

|

135

|

- The employer shall be liable for the payment of the tax required to be

deducted and withheld under this chapter, and shall not be liable to any

person for the amount of any such payment.

|

|

136

|

- YOU BET YOUR SWEET ASS IT

IS !

- HERE AGAIN, WE SEE THAT IT IS

THE TAX COLLECTOR, THE EMPLOYER, WHO IS ACTUALLY THE “PERSON” MADE

LIABLE BY THE STATUTES FOR THE PAYMENT OF THE INCOME TAX IN SUBTITLE C.

JUST LIKE IT WAS THE “WITHHOLDING

AGENT “, ALSO A TAX COLLECTOR, THAT WAS THE “PERSON” MADE LIABLE

FOR THE PAYMENT OF THE INCOME TAX IN SUBTITLE A !

|

|

137

|

- So, IF YOU ARE NOT REALLY LIABLE

FOR INCOME TAX (UNDER SECTION 1461), WHY IS YOUR EMPLOYER WITHHOLDING IT

FROM YOU ?

|

|

138

|

- (p) Voluntary withholding agreements

- …

- (3) Authority for other voluntary withholding

- The Secretary is authorized by regulations to provide for withholding—

- (A) from remuneration for services performed by an employee for the

employee’s employer which (without regard to this paragraph) does not

constitute wages, and

- (B) from any other type of payment with respect to which the Secretary

finds that withholding would be appropriate under the provisions of this

chapter,

|

|

139

|

- (p) Voluntary withholding agreements

- …

- if the employer and employee, or the person making and the person

receiving such other type of payment, agree to such withholding. Such

agreement shall be in such form and manner as the Secretary may by

regulations prescribe. …

|

|

140

|

- (p) Voluntary withholding agreements

- Did they tell you this was voluntary (an Allowance – like it says), or

did they ignore the title of the Form and lie to you and tell you this was mandatory for “employment”.

|

|

141

|

- DID YOU NAIVELY ALLOW THEM TO

WITHHOLD TAX THAT YOU DON’T REALLY HAVE

TO PAY, BECAUSE YOU ARE NOT LIABLE FOR THE PAYMENT OF IT UNDER

THE LAW ?

|

|

142

|

- Are they intentionally taking

advantage of you through your trusting nature and lack of accurate

information regarding the limits of the federal taxing powers ?

|

|

143

|

|

|

144

|

|

|

145

|

- … Our legal right to ask for

information is Internal Revenue Code sections 6001, 6011, and 6012(a)

and their regulations. They say that you must file a return or statement

with us for any tax you are liable for. …

|

|

146

|

- Every person liable for any

tax imposed by this title, or for the collection thereof, shall keep

such records, render such statements, make such returns, and comply with

such rules and regulations as the Secretary may from time to time

prescribe….

|

|

147

|

- (a) General rule. When

required by regulations prescribed by the Secretary any person made

liable for any tax imposed by this title, or with respect to the

collection thereof, shall make a return or statement according to the

forms and regulations prescribed by the Secretary…

|

|

148

|

|

|

149

|

- (a) If any person liable to pay any tax

neglects or refuses to pay the same, after demand, the amount (including

any interest, additional amount, addition to tax, or assessable penalty,

together with any costs that may accrue in addition thereto) shall be a

lien in favor of the United States upon all property …

|

|

150

|

- (a) Authority of Secretary.

- If any person liable to pay any

tax neglects or refuses to pay the same within ten days after notice and

demand, it shall be lawful for the Secretary to collect such tax … by

levy upon ...

|

|

151

|

- Any person required under this

title to pay any estimated tax or tax, or required by this title or by

regulations made under authority thereof to make a return, keep any

records, or supply any information, who willfully fails to pay such

estimated tax or tax, make such return, keep such records, or supply

such information, at the time or times required by law or regulations,

shall, in addition to other penalties provided by law, be guilty of a

misdemeanor…

|

|

152

|

- The only people required to pay income tax are those that are liable for

tax under Sections 1461 and 3403.

- The only people required to file a 1040 return are those persons,

according to Section 6001 and 6011, that are liable for tax or the collection

thereof (like Employers and “Withholding Agents”, and non-resident

aliens and foreign corporations under T.D. 2313)

|

|

153

|

- (a) General rule. Returns with

respect to income taxes under subtitle A shall be made by the following:

- (1)(A) Every individual having

for the taxable year gross income which equals or exceeds the exemption

amount, except that a return shall not be required of an individual - …

|

|

154

|

- (a) General definition. Except as

otherwise provided in this subtitle,

gross income means all

income from whatever source derived,

including (but not

limited to) the following items:

- (1) Compensation for services, including

fees, commissions,

fringe benefits

and similar items;

- (2) Gross income derived from business;

- (3) Gains derived from dealings in

property;

- (4) Interest;

- (5) Rents;

- (6) Royalties;

- (7) Dividends;

- (8) Alimony and separate maintenance

payments;

- (9) Annuities;

- (10) Income from life

insurance and endowment contracts;

- (11) Pensions;

- (12) Income from discharge

of indebtedness;

- (13) Distributive share of

partnership gross income;

- (14) Income in respect of a

decedent; and

- (15) Income from an

interest in an estate or trust.

|

|

155

|

|

|

156

|

|

|

157

|

- And just how is Section 22 (and

subsequently Section 61) enabled under the law ?

|

|

158

|

|

|

159

|

- Part

- 500 [Reserved]

- 501 Australia .................

- 502 Greece ...................

- 503 Germany ................

- 504 Belgium ..................

- 505 Netherlands ............

- 506 Japan .....................

- 507 United Kingdom ......

- 509 Switzerland ............

- 510 Norway ..................

|

|

160

|

- Part 519 is the Canadian Tax

Treaty. Section 61 actually

defines the sources of taxable income under the 75 year tax treaty with

Canada that was signed in 1918 and lasted until 1993. This is because of

the limited implementation of Section 61, inherited from Section 22

under the 1939 code, which was carried forward, according to the

footnote, “substantially unchanged”.

|

|

161

|

- Section 61 does not define the domestic sources of a Citizen’s taxable

income at all. As far as citizens

are concerned, Section 61 only defines the Canadian sources of taxable

gross income under the Canadian Tax Treaty.

- Which agrees with everything else in the law that we have seen regarding

subtitle A income tax being a foreign tax in the form of a tariff,

exactly as it was identified by

the Supreme Court in the Brushaber Opinion in 1916!

|

|

162

|

- The Criminal Investigative

Division enforces the criminal statute applicable to income, estate,

gift, employment, and excise tax laws (other than those excepted in IRM

1112.51) involving United States Citizens residing in foreign countries and

nonresident aliens subject to Federal income tax filing requirements. …

(emphasis added)

|

|

163

|

|

|

164

|

- Lets look at the original provisions of the legislation enacted; the

Underwood–Simmons Tariff Act of Oct. 3, 1913.

- Please NOTE HOW the “United States” is defined in Section H for use in

carrying out this tariff legislation?

|

|

165

|

|

|

166

|

|

|

167

|

- Here, we see that the “United States “

is defined as the territories and possessions FOR USE IN CARRYING

OUT THE PROVISIONS OF THIS TARIFF ACT, because a tariff tax CANNOT and DOES

NOT APPLY in the fifty states to citizens – ONLY

IN THE TERRITORIES AND POSSESSIONS where the Federal government

is the Sovereign, and the Constitution does not apply.

|

|

168

|

- 7701(a) …

- (9). United States. The term

''United States'' when used in a geographical sense includes only the

States and the District of Columbia.

|

|

169

|

- (5) State

The term ''State'' means -

(A) any of the 50 States, the District of Columbia, the

Commonwealth of Puerto Rico, the Virgin Islands, the Canal Zone, Guam,

American Samoa, and the Commonwealth of the Northern Mariana Islands,

and ...

|

|

170

|

- SO, CAN CONGRESS WRITE LAWS THAT ARE SIMPLE AND CLEAR ?

- IS THERE ANY CONFUSION ABOUT WHAT IS ACTUALLY WRITTEN IN THE LAW?

- SHOULDN’T WE TELL SOMEBODY WHAT WE NOW KNOW ?

- DON’T WORRY, THEY ARE NOT LISTENING !

|

|

171

|

- THE STATUTES, UNDER THE ACTUAL LEGISLATION

OF THE UNDERWOOD –SIMMONS TARIFF ACT ENACTED IN 1913, LAY AN

INCOME TAX:

- 1. ON FOREIGN ACTIVITY IN THE FIFTY STATES,

- 2. ON ALL ACTIVITY IN THE TERRITORIES & POSSESSIONS (Where the

federal government MAY

TAX DIRECTLY as the Sovereign because the CONSTITUTION does not

apply), and

- 3. ON A CITIZEN’S ACTIVITY IN A

FOREIGN COUNTRY UNDER A TAX TREATY (Sec. 61, 1918)

|

|

172

|

- AND IF YOU DON’T VOLUNTARILY FILE

A FORM 1040 RETURN, WHAT CAN THE I.R.S. LAWFULLY ASSESS AGAINST YOU ?

|

|

173

|

|

|

174

|

- ARE INCOME TAXES PAID BY STAMP

!!!

|

|

175

|

- AS ENFORCED BY THE IRS, THE INCOME TAX IS NEITHER UNIFORM AS AN INDIRECT

TAX, NOR IS IT APPORTIONED AS A

DIRECT TAX, AND THEREFORE, THE ENTIRE ENFORCEMENT OPERATION OF THE IRS

AMOUNTS TO NOTHING MORE THAN AN UNCONSTITUIONAL OPERATION DESIGNED TO REDUCE

YOU, THE TRUE AMERICAN SOVEREIGN, TO THE SERVILE STATUS OF A CONQUERED

SUBJECT, THAT OF A VIRTUAL FEDERAL PEON.

|

|

176

|

- WHAT ELSE DOES THE SUPREME COURT

SAY ABOUT FEDERAL TAXATION THAT IS RELEVANT ?

|

|

177

|

- “There is no safety in allowing

the limitation to be adjusted except in strict compliance with the

mandates of the constitution, which require its taxation, if imposed by

direct taxes, to be apportioned among the states according to their

representation, and, if imposed by indirect taxes, to be uniform in

operation and, so far as practicable, in proportion to their property, equal

upon all citizens...” Pollock v.

Farmer’s Loan & Trust Co., 157 U.S. 429, 607 (1895)

|

|

178

|

- “The inherent and fundamental

nature and character of a tax is that of a contribution to the support

of the government, levied upon the principle of equal and uniform

apportionment among the persons taxed, and any other exaction does not

come within the legal definition of a 'tax’.” Pollock v. Farmer’s Loan

& Trust Co., 157 U.S. 429, 599 (1895)

|

|

179

|

- Now remember, disingenuous

government officials, attorneys and judges will try to tell you that the

16th Amendment defeated and effectively overturned the Pollock

ruling (ignoring Eisner in 1920).

BUT, you have just seen that the Supreme Court clearly rejected

that claim and argument, plainly and completely.

|

|

180

|

- The decisions do not contradict or reverse each other – they operate

harmoniously together, hand in hand to each properly address a different

aspect of the constitutional federal taxing powers.

- Pollock (1896) & Eisner (1920) uphold the Constitutional prohibition

on direct taxation without apportionment.

- Brushaber & Stanton (both 1916) uphold the federal power to tax Indirectly,

in the form of an impost (tariff).

|

|

181

|

- “There is no such thing in the

theory of our national government as unlimited power of taxation in

congress. There are limitations, as he justly observes, of its powers

arising out of the essential nature of all free governments; there are

reservations of individual rights, without which society could not

exist, and which are respected by every (legitimate) government. The

right of taxation is subject to these limitations. Pollock v. Farmer’s

Loan & Trust Co., 157 U.S. 429, 599 (1895)

|

|

182

|

- BUT NOT ANY MORE !

- NOW THEY CAN TAKE 100 PERCENT

IF THEY WANT (THEY CLAIM), AND THERE IS NOTHING YOU CAN DO ABOUT IT.

- IS THIS REPRESENTATIVE GOV’T ?

- IS THIS LIMITED GOVERNMENT ?

- OR, IS THIS THE TYRANNY OF AN OMNIPOTENT STATE that the

Constitution was written to forever prohibit ?

|

|

183

|

- AND WHAT ARE THEY REALLY

DOING ?

|

|

184

|

- 1. Abolition of property in land and the application of all rents of

land to public purposes. (Bail

Out)

- 2. A heavy progressive or graduated income tax.

- 3. Abolition of all rights of inheritance. (estate tax)

- 4. Confiscation of the property of all emigrants and rebels. (DEA, IRS,

ATF)

- 5. Centralization of credit in the hands of the state, by means of a

national bank with State capital and an exclusive monopoly. (Federal

Reserve)

|

|

185

|

- AND WHAT DID THE FOUNDING FATHERS

SAY ABOUT TAXES LIKE THE INCOME TAX ?

|

|

186

|

- “A wise and frugal government …shall not take from the mouth of labor

the bread it has earned.”

- Thomas Jefferson

First Inaugural Address

|

|

187

|

- “If we can prevent the government from wasting the labors of the people

under the pretense of taking care of them, they must become happy."

Thomas Jefferson to Thomas Cooper, 1802.

|

|

188

|

- “If a nation expects to be

ignorant and free in a state of civilization, it expects what never was

and never will be...

if we are to guard against ignorance and remain free, it is the

responsibility of every American to be informed”

|

|

189

|

- ARE WE LIVING UP

TO HIS CHARGE

TO US?

- Many Of US say NO!

- What do you think?

|

|

190

|

- AND WHAT DOES THE BIBLE SAY ABOUT PROPER TAXATION ?

|

|

191

|

- 25 Jesus prevented him, saying, What

thinkest thou, Simon ?

Of whom do the kings of the earth take custom or tribute (tax)?

Of their own children, or of strangers (foreigners) ?

- 26 Peter saith unto him, of strangers.

Jesus saith unto him,

“THEN THE CHILDREN ARE FREE”.

Mathew 17:25-26

|

|

192

|

- Stand fast therefore in the

liberty wherewith Christ hath made us free, and be not entangled again

with the yoke of bondage.

John 8:32, Acts 15:10,

Romans 6:18

- Ye SHALL KNOW THE TRUTH and

- THE TRUTH WILL SET YOU FREE!

|

|

193

|

- DO NOT ENSLAVE YOUR OWN CHILDREN IN

THE NAME OF TAX !

|

|

194

|

- TAX THE

FOREIGN PRESENCE IN

YOUR LAND !

|

|

195

|

- So, now that you

know the TRUTH

about Income Tax,

Do you believe in the Communist Manifesto,

or the Constitution !

|

|

196

|

- “Here I close my opinion. I

could not say less in view of questions of such gravity that go down to

the very foundation of the government. If the provisions of the

constitution can be set aside by an act of congress, where is the course

of usurpation to end ?

|

|

197

|

- The present assault upon capital

is but the beginning. It will be

but the stepping-stone to others, larger and more sweeping, till our

political contests will become a war of the poor against the rich,-a war

constantly growing in intensity and bitterness.

|

|

198

|

- If the court sanctions the

power of discriminating taxation, and nullifies the uniformity mandate

of the constitution,' as said by one who has been all his life a student

of our institutions, 'it will mark the hour when the sure decadence of

our present government will commence.' If the purely arbitrary

limitation of four thousand dollars in the present law can be sustained,

|

|

199

|

- none having less than that

amount of income being assessed or taxed for the support of the

government, the limitation of future congresses may be fixed at a much

larger sum, at five or ten or twenty thousand dollars, parties

possessing an income of that amount alone being bound to bear the

burdens of government; or the limitation may be designated at such an

amount as a board of 'walking delegates' may deem necessary.

|

|

200

|

- There is no safety in allowing

the limitation to be adjusted except in strict compliance with the

mandates of the constitution, which require its taxation, if imposed by

direct taxes, to be apportioned among the states according to their

representation, and, if imposed by indirect taxes, to be uniform in

operation and,

|

|

201

|

- so far as practicable, in

proportion to their property, equal upon all citizens. Unless the rule

of the constitution governs, a majority may fix the limitation at such

rate as will not include any of their own number.” Pollock v. Farmer’s Loan & Trust

Co., 157 U.S. 429, 607 (1895)

|

|

202

|

- (a) General rule

…. the gross amount of all taxes and revenues received under the

provisions of this title, and collections of whatever nature received or

collected by authority of any internal revenue law, shall be paid daily

into the Treasury of the United States under instructions of the

Secretary as internal revenue collections, by the officer or employee

receiving or collecting the same, without any abatement or deduction on

account of salary, compensation, fees, costs, charges, expenses, or

claims of any description

|

|

203

|

- BUT, If you look at the back of

the last check you sent in to the IRS, you will see who is really

getting our money, our supposed tax dollars. It says:

- “pay to any F.R.B.”

|

|

204

|

- WHY is the Federal Reserve Bank

cashing your tax check instead of the U.S. Treasury, as required by law

?

|

|

205

|

- ARE YOU BEING FORCED TO PAY SOMEONE ELSE’S DEBTS ?

(the government’s) ?

|

|

206

|

- WHERE IS THAT IN EITHER THE LAW, OR

THE CONSTITUTION ?

|

|

207

|

- THEN, is it EVEN REALLY TAX ?

- Why then, is there no record at the Treasury in your name, of tax being

paid after the employer takes the money from your pay and sends it

in? Nor is there even any credit

in your name for the payment of any tax until you file a Form 1040!

- HOW IS THAT? WHY IS THAT ?

|

|

208

|

- AND WHY ?

- Title 31 U.S.C. 5103. Legal tender.

- United States coins and

currency (including Federal reserve notes and circulating notes of

Federal reserve banks and national banks) are legal tender for all

debts, public charges, taxes, and dues. Foreign gold or silver coins are

not legal tender for debts.

|

|

209

|

- “He has erected a multitude of New Offices, and sent hither swarms of

Officers to harass our people and eat out their substance.”

|

|

210

|

- Well then, if you care about

America, her Freedom, her children, and her future (and theirs), help us

spread the word and help make all Americans aware of the TRUTH that you

have just learned. Please, tell

your family and friends about this

“Learn The Law in 90 Minutes” slide show and urge them to watch

it. When enough people know the

TRUTH, the tyranny will end.

- www.Tax-Freedom.com

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}